Monetary policy and High Prices

Despite public opinion polls consistently showing price increases as one of the top five most critical issues facing the population, consumer prices have evolved into a politically charged topic over the last few months. This culminated in the establishment of a parliamentary committee tasked with reviewing price-formation structures and sparked several televised debates. Yet, the problem remains unresolved. The growth rate of consumer prices has accelerated once again in recent months.

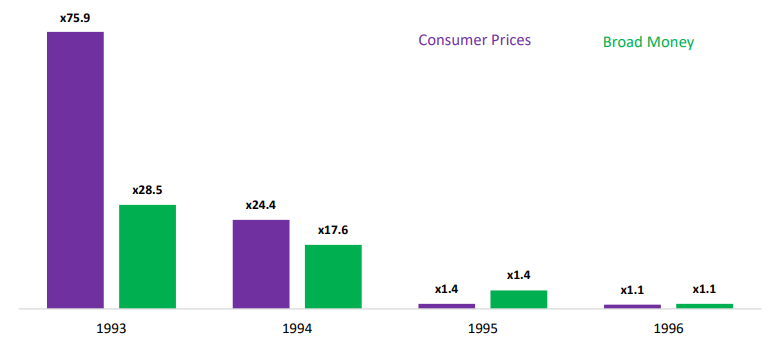

Price growth in Georgia is a historically problematic issue rooted in a fundamental cause: hyperinflation. Following the introduction of the Georgian coupon in 1993 and its subsequent rapid overprinting, consumer prices experienced four-digit growth. Within a year of the coupon’s launch, cash and broad money supplies expanded 152-fold and 130-fold, respectively. Consequently, annual inflation reached 7,487.9% in 1993 and stood at 6,473.9% the following year.

Chart 1: Annual Inflation and Broad Money Dynamics

Source: International Monetary Fund

Although this was followed by a so-called stabilization period, marked by the introduction of the Lari (GEL) as the national currency and a clear constitutional mandate for price stability was given to the National Bank of Georgia (NBG), increases in the general price level of the economy remained perennially problematic. More often than not, the central bank sidelined its primary mandate - price stability - leading to a rise in the aggregate price level across the economy. While not reaching the four-digit figures of the 1990s, several periods of double-digit inflation over the last few decades clearly indicate this.

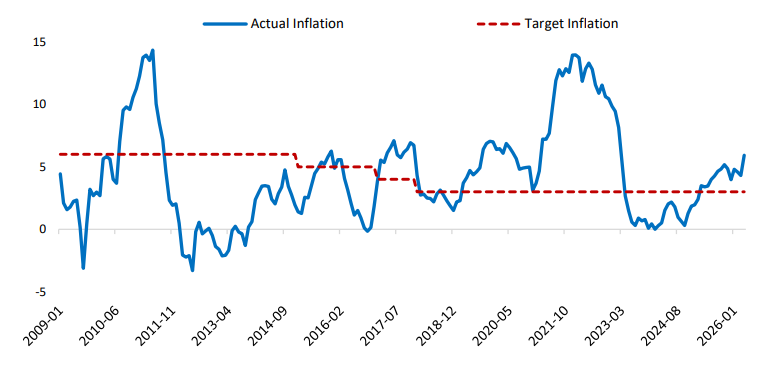

Historically, inflation trends demonstrate sharp deviations from targeted indicators, highlighting the central bank's failure to deliver on its primary responsibility: ensuring price stability. The central bank states that it “maintains price stability by ensuring a low and predictable inflation rate”. Low inflation implies keeping medium-term changes in the Consumer Price Index (CPI) aligned with target figures. Predictability denotes inflation dynamics that demonstrate minimal variance and low volatility relative to that medium-term target. However, inflation dynamics in Georgia clearly illustrate that the National Bank fails to ensure low and predictable inflation; the inflation rate fluctuates noticeably, misses the target indicator most of the time, and deviates from it significantly.

Chart 2: Annual Change in the Consumer Price Index (CPI)

Source: National Statistics Office of Georgia

This trend persists today. As of April, of this year, the annual increase in consumer prices reached 5.9%, exceeding the current inflation target of 3%. Given the policies pursued prior to this period, an acceleration of inflation was to be expected. In April’s inflation breakdown, a particularly high contribution of 2.6 percentage points came from the food and non-alcoholic beverages commodity group. The latter represents the largest single component of the consumer basket.

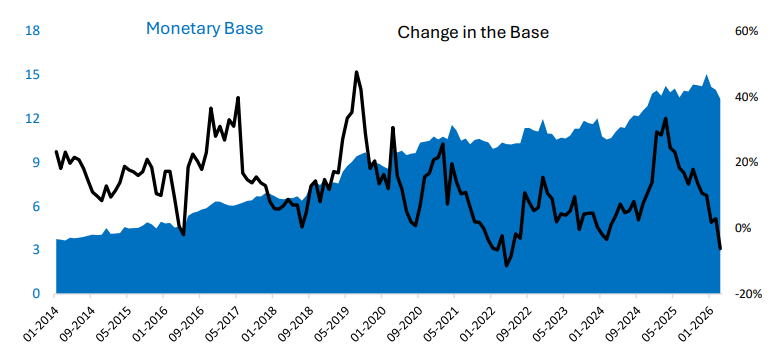

The root cause of price instability, both now and in the past, lies within the policies of the National Bank. Therefore, resolving this issue requires an overhaul of central bank policy rather than altering the functions of any other public institution. More precisely, shifts in the general price level are a consequence of changes in the money supply (at least over the long term). The money supply within the economy is determined by the monetary base, which is under the complete control of the central bank. The National Bank's policy directly impacts the monetary base, where growth in the monetary base indicates an expansionary central bank policy, and a decrease indicates the opposite.

Chart 3: Monetary Aggregate and Growth Rate, Billion GEL and %

Source: National Bank of Georgia

The current acceleration of inflation was preceded by a rise in the growth rate of the monetary base. This pattern mirrors previous periods, as current inflation is a lagging result of past policy decisions. This time, however, the National Bank utilized primarily unconventional instruments to fuel monetary expansion. Foremost among these were foreign exchange interventions, the scale and frequency of which have grown significantly in recent years. Foreign exchange interventions, specifically, buying US dollars on the domestic market, affect the nominal exchange rate of the Lari in the short run and translate into inflation down the line. Under other equal conditions, the central bank's purchasing of dollars on the market triggers a depreciation of the Lari against the dollar, while the resulting Lari emission causes a rise in the overall price level of the economy in the future.

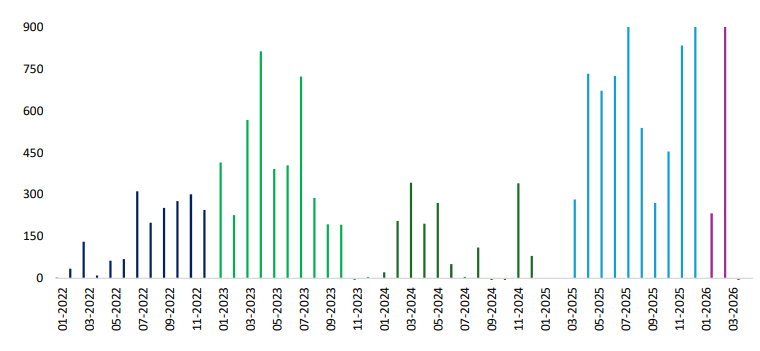

Chart 4: Net Foreign Exchange Interventions, Million GEL

Source: National Bank of Georgia

Ever since the post-pandemic period, the National Bank has been actively absorbing foreign currency (USD) entering the economy to accumulate reserves. In doing so, it artificially restrains the nominal appreciation of the Lari in the present, while simultaneously fostering a higher aggregate price level down the road. Between 2022 and 2024, the National Bank’s USD purchases on the foreign exchange market injected 6,971.7 million GEL into circulation, equivalent to 44.6% of the broad money supply available at the start of that period. Over the subsequent period, Lari emissions accelerated via these foreign exchange interventions: in 2025 alone, the central bank bought foreign currency worth 6,619.7 million GEL. This purchase represented an emission volume equal to 24.6% of the broad money supply at the beginning of that year. Furthermore, in the first quarter of the current year, the National Bank has already purchased foreign currency worth 1,340.5 million GEL.

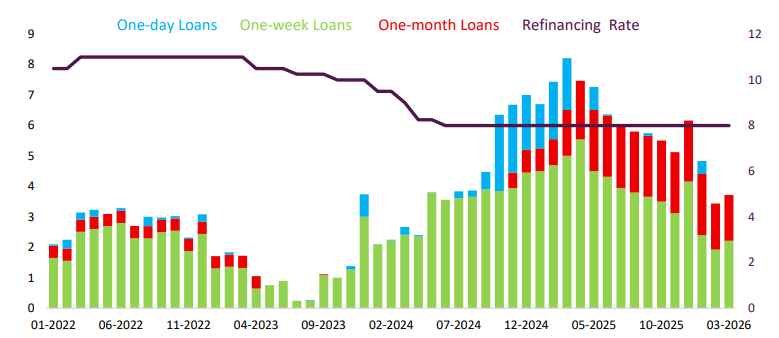

Chart 5: Open Market Operations and the Refinancing Rate, Million GEL and %

Source: National Bank of Georgia

While foreign exchange interventions remain dominant, the central bank has also actively used conventional monetary instruments to accelerate the money supply. The National Bank notes that its primary tool for maintaining price stability is the refinancing rate, which represents the cost of open market operations (one-week and one-month loans extended by the National Bank to commercial banks). A lower refinancing rate makes borrowing Lari liquidity from the National Bank more attractive for commercial banks, accelerating the money supply. Since 2023, the National Bank has been cutting its refinancing rate, driving up the volume of one-week and one-month loans issued to commercial banks.

Therefore, the National Bank has recently pursued an expansionary monetary policy using both conventional and unconventional instruments, setting the stage for an accelerated rate of price increases now and in the future. Both historically and now, the underlying cause of price instability is the central bank’s pro-inflationary monetary policy. Overcoming the challenges presented by a rising aggregate price level can only be achieved by changing monetary policy and strengthening oversight of the institution responsible for managing it.

For the complete document, including relevant sources, links, and explanations, please see the attached file.